SMALL BUSINESS AND A BIG VISION — A GUIDE TO PLANNING FOR RETIREMENT

--

Retirement planning is a great way to save and secure for your future. Despite small businesses employing nearly half of the American workforce, only 53% provide retirement plans. Employers can support their workers through a range of options — starting from financial education going all the way to a traditional 401(k) plan. Providing these opportunities not only enhances employee attraction and retention but underscores a commitment to employee well-being.

If you as an employer choose, we have recommended some options for retirement plans that work for small businesses, including education, SIMPLE IRAs, SEP IRAs, and 401(k).

Securing A Financial Future: Educate Employees

Small businesses do not need to rely on plans to prepare their workers for retirement. Employers can still help employees secure financial stability for their future by providing education for their employees. This would allow employees to make their own decisions in terms of retirement and utilize different investment plans. Educating employees can look like:

1. Host retirement workshops with financial experts, covering saving strategies, investments, and emphasizing early planning for a comprehensive retirement approach.

2. Offering resources such as sharing informative materials on retirement plans, investments, and financial management, such as fact sheets or webinars. Two examples can be found here and here.

3. Educating employees on making their own IRAs and doing so in an automated way can empower them to control their own future. Check out this link for more information on Robo-Advisors as an important tool.

Decoding IRA-Based Plans: Pros and Cons for a Balanced Retirement Approach

1. Simplified Employee Pension (“SEP”)

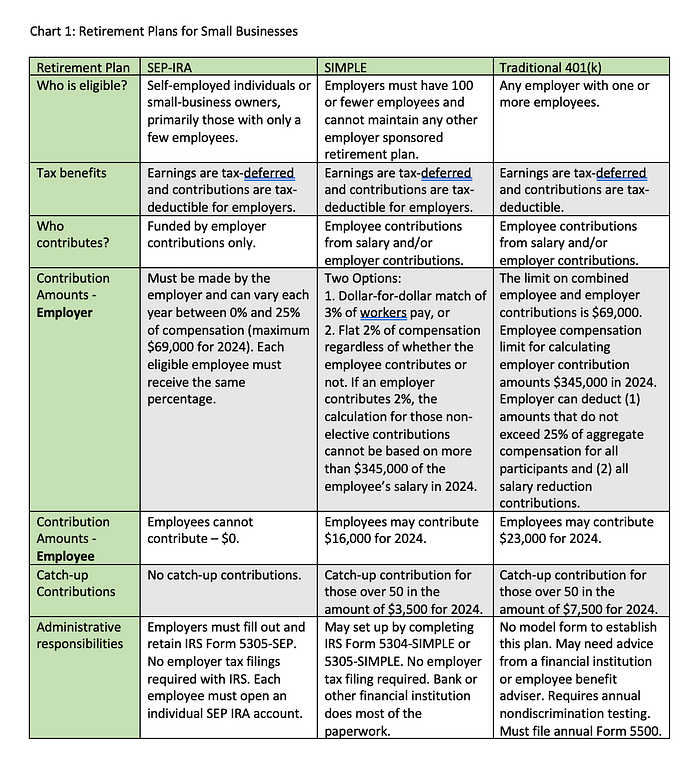

A SEP allows employers to set up SEP IRAs for themselves and each employee. Currently, the contribution limit is up to 25% of the employee’s total compensation with a maximum of $69,000 for 2024. This plan is unique in that only employers can contribute to their employees’ retirement savings. This type of plan works great for sole proprietors or businesses with only a few employees. This is a popular choice for small businesses because it is relatively easy to set up and maintain. It’s a flexible tax-advantaged way for businesses to provide retirement benefits for themselves or their employees.

Advantages

· Easy to set up: Has a low start-up cost and can be set up in three steps by employers. This can be streamlined further by working with a bank or qualified financial institutions.

· Flexible employer contribution amounts: It’s possible to change contribution rates from one year to the next — offering flexibility when business conditions vary. Visit Chart 1 to see contribution amounts for 2024.

· Unique to the SEP is the ability to use it in addition to another retirement plan. For the self-employed, pairing a SEP IRA with another IRA or a 401(k) plan can maximize contributions and savings.

Disadvantages

- No catch-up contributions: While employees over 50 have higher contribution limits to “catch up” before retirement on other plans, this isn’t an option with SEP IRAs.

- Only employers can contribute to their employees’ retirement savings.

2. Savings Incentive Match Plan for Employees (“SIMPLE-IRA”)

A SIMPLE IRA is a retirement plan that is designed for small businesses with 100 or fewer employees who received $5,000 or more in compensation from you for the preceding year. Employees can contribute up to $16,000 in 2024. Meanwhile, employer contributions are mandatory for SIMPLE IRAs, and they can be made in one of two ways. An employer can contribute a nonelective 2% of employee compensation with an annual salary limit of $345,000 in 2024 (meaning a contribution cap of $6,900) or an elective contribution of up to 3% dollar-for-dollar match provided the employee contributes at least this amount themselves with no salary cap.

To exemplify how a SIMPLE operates, imagine you have an annual salary of $60,000 and work for a company that takes advantage of a SIMPLE IRA. The first option is that the company matches up to 3% of what the employee contributes. You decide to contribute 6% of your salary for a total of $3,600. Since the company matches up to 3%, employer contribution will be $1,800. This is because the maximum match is capped at 3% even though you contributed 6%. Alternatively, your employer can use a 2% nonelective contribution. The employer contributes 2% of your salary, which would be $1,200 ($60,000 x 2%). The key difference between these options is that the employer contribution depends on your contribution. In the nonelective scenario, the employer contributes 2% regardless of whether you contribute.

SIMPLE IRAs typically have lower administrative costs and burdens. However, there are restrictions on the amount that can be contributed compared to some other retirement plans, making it a more accessible option for smaller companies.

Advantages:

· Easy to set up: Can be set up with easy steps and with lots of investment options.

· Flexible Contributions: Both employers and employees can make contributions.

· Employees over 50 can make catch-up contributions to their accounts.

Disadvantages:

· You must consider all employees employed at any time during the calendar year regardless of whether they are eligible to participate.

· Once the business has over 100 employees, you can no longer maintain the SIMPLE plan.

A Closer Look at Defined Contribution Plans

1. Traditional 401(k)

A traditional 401(k) retirement plan is a tax-advantaged savings plan that allows employees to contribute a portion of their pre-tax income to individual accounts. The 401(k) contribution limit for 2024 is $23,000 for employee contributions and $69,000 for the combined employee and employer contributions. It also offers the business the most flexibility in plan design. However, it does come with some administrative tasks and costs not generally present in other plans. Employers have the option to make contributions to employees’ 401(k) accounts through options such as matching contributions.

Advantages

- Maximizes contribution amounts: Contributions are made before any income taxes are calculated. Though you’ll pay taxes on distributions down the line, you’re maximizing the amount in the retirement plan that generates interest.

· Automatic enrollment options: This feature is designed to encourage employee participation by enrolling eligible employees automatically in the 401(k) plan.

· If you’re age 50 or older, you’re eligible for an additional $7,500 in catch-up contributions, raising your employee contribution limit to $30,500.

Disadvantages

- Costs: There are administrative costs associated with setting up and maintaining the plan. Small businesses should consider the overall costs.

- Compliance: 401(k) plans must comply with IRS regulations, including nondiscrimination testing to ensure that benefits are not disproportionately favoring highly compensated employees.

Conclusion

Navigating the landscape of retirement plans for small businesses requires careful consideration and strategic decision-making. Choosing the right retirement plan for your small business involves more than just numbers; it’s a strategic journey. In this exploration, we’ve delved into the diverse world of retirement options, from SIMPLEs and SEPs to 401(k)s. By aligning your business’s needs with the goals of your employees, you can chart a course for a prosperous future. Get ready to navigate the retirement landscape with confidence!

Jasmin Sethi is the CEO of Sethi Clarity Advisers. She educates investors on the topic of building a secure retirement through a variety of asset classes. She assesses the implications of various policy and industry changes on individual opportunities for building a retirement portfolio and facilitate better outcomes for individual financial security.

Olivia Matteo is a 3L at Fordham Law School and a Research Associate at SCA.